'Tis The Season To Learn About The Economy | (12/1/22)

"A nickel ain’t worth a dime anymore." - Yogi Berra

What You Need To Know Today:

• The Bureau of Economic Analysis released updated Core Personal Consumption Expenditures (PCE) Consumer Price Index (CPI) data, which measures the change in the price of goods and services purchased by consumers, excluding food and energy, and is the Fed’s primary inflation gauge. The reading came in at 0.2% month-over-month, lower than the pre-report market expectation of 0.3%.1 This is technically good and tells us that inflation is heading in the right direction (down). Interest rates will follow as this continues month to month.

TL;DR — Inflation is slowly being curbed.

• Initial Jobless Claims, which measure the number of individuals who filed for unemployment insurance for the first time during the past week and also serves as an important signal for overall economic health, came in better than expected. According to the Department of Labor, there were 225,000 new “first-time” unemployment claims last week, which was lower than the forecasted market expectation of 234,000 and 16,000 lower than the last reading.2 It is worth noting that if it hadn’t been Thanksgiving last week the number of new claims would have likely been higher.

TL;DR — Initial Jobless Claims are down, lower than expected.

• Leveraged Loans are commercial loans structured, arranged, and administered by one (or several) commercial or investment banks and then sold (or syndicated) to other banks and institutional investors. In general, leveraged lending is important because it is the “key player” for mergers and acquisitions, business recapitalization/refinancing, equity buyouts, and business/product expansions. While I won’t get too in the weeds on leveraged loans today, I would like to note that across the institutional lending space there has been a lot of chatter about leveraged loan issuance stalling in 2022 — likely due to the increased cost of capital. However, according to S&P LCD Research, this is only the case for “institutional” deals — which are “riskier, non-amortizing term debt” purchased by alternative credit managers (CLOs). Looking at pro-rata (proportional) issuance including amortizing loans and revolving credits mostly held by banks — new issuance is up 22% vs 2021.3

TL;DR — Despite the increased cost of capital, businesses are still taking on more debt.

Chart Of The Day:

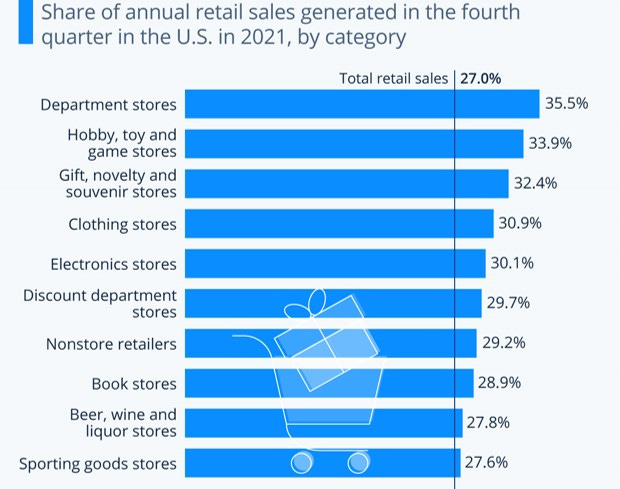

Most people assume that the Holiday season (Q4) is the most significant time of year for retail sales in the United States. Are they correct? According to retail sales figures published by the U.S. Census Bureau, the answer is yes. However, it is certainly more significant for some types of retailers than it is for others.

If you were to distribute the expected “weight of sales” by quarter (assuming all quarters were equal) each quarter should represent 25% of a given year’s total sales. As Illustrated by the below data, some types of retailers are far beyond that including department stores, hobby/toy/game stores, and general gift/novelty/souvenir stores which all have more than 32% of their sales coming in Q4. Meanwhile, retailers such as beer/wine/liquor distributors and sporting goods stores see ~28% of their annual sales in Q4 — just 3% more than what the previously mentioned even distribution (25%) would look like.

TL;DR: Holiday season sales are massively significant for some but less significant for others than “conventional wisdom” might have you think.

Just How Important is the Holiday Season for Retailers?4

Source: Bureau of Economic Analysis

Source: Department of Labor

Source: LCD Research